Most robbery is done in the dark. More daring robbery in the day usually requires a disguise.

Pirates had patches over one eye. Stagecoach robbers in cowboy films had their neckerchiefs pulled up over their faces. Modern day jewellery thieves and bank robbers usually go to the trouble of donning a balaclava for their heists.

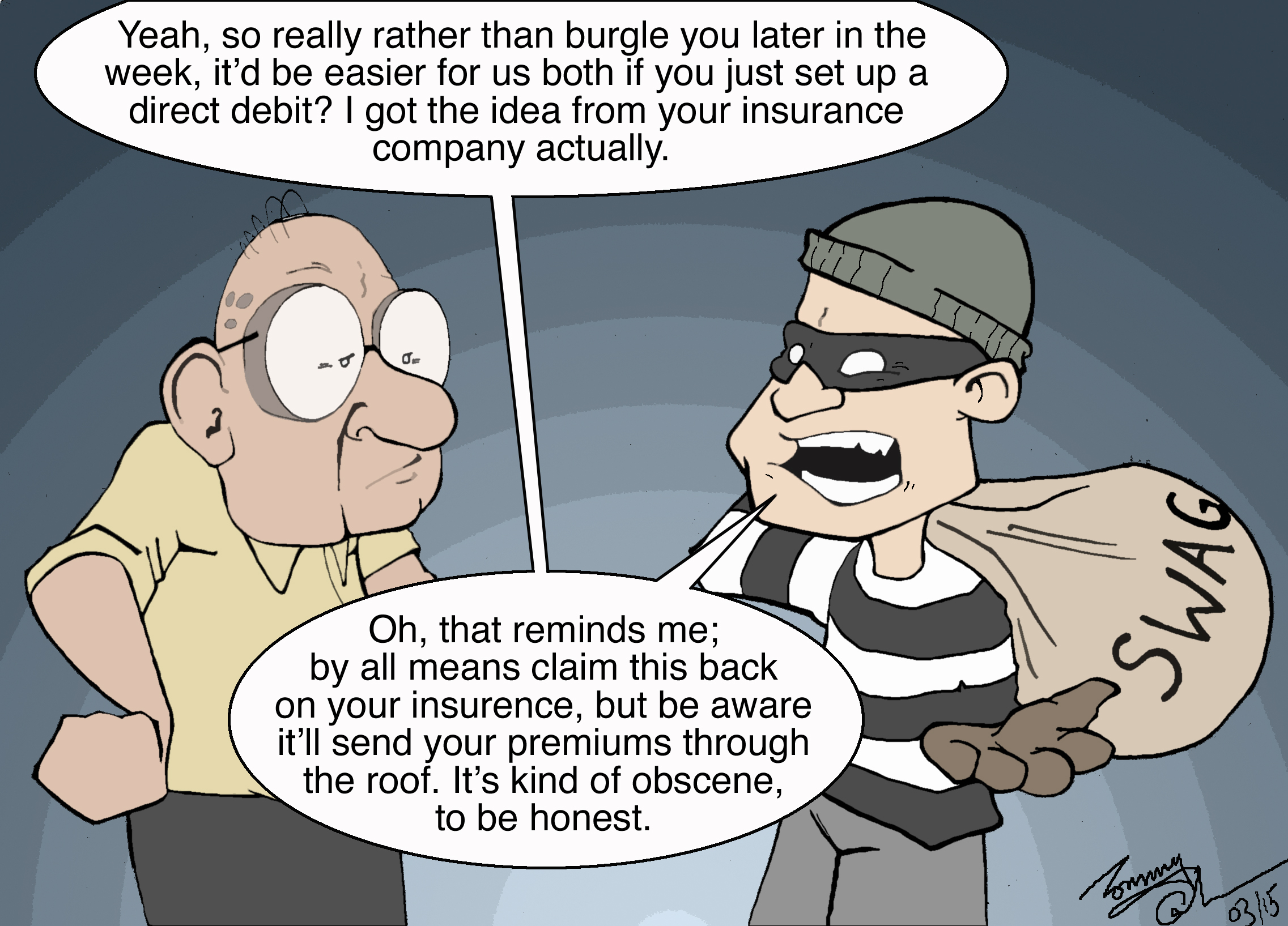

Today’s insurance salesmen are much more brazen, particularly with older people. They come well dressed in grey suits; they don’t bother with a disguise, they hide behind their “trusted” brand.

A recent report in Times Money covered the cases of a number of elderly people who found they were paying way over the top for insurance renewals.

An 89 year old was paying five times as much as new customers for building insurance. When they were finally exposed after the man had died, Lloyds merely pointed out that the man “could have cancelled his insurance at any time”. Not so much a trusted friend as buyer beware !

In another example, a daughter found her mother was paying more than twice the going rate for house insurance. After they were rumbled, Aviva claimed it was a “miscalculation”.

It appears there are many more examples like this where insurance companies exploit the fact that at renewal time, elderly people are less likely to shop around and switch providers. Most older people are used to being able to trust their insurance company to treat them well. It now seems that trust maybe misplaced.

Who knows what they will be upto next ?

I find the web and the small print difficult to compare ‘Like with Like’. I much prefer a written quotation to compare against a written quotation: Again it would appear that some of the trusted sellers like your friendly courteous high street retails, and union associations while they may offer headline reduced rates, when one receives the package it is often, underwritten by one of the larger insurance group of companies- which I find misleading Personally! As has been pointed out one pays ones money and one takes a chance? Life is not simple and loyalty does not buy you bonus points from year to year, as my older family aunts and uncles used to encourage, for a more equitable cover for that reduced premium.

Once again someone has rattle my cage, and engaged brain?

This blog makes me wonder of my previous life working for a mutual insurance company on the Fish Docks.

In principal all the members has a common interest: A fishing vessel, to reduce costs they formed a mutual insurance company that insured each vessel for a an insured sum of a ‘declared’ hazard’ This was paid out by the mutual company to the affected insured vessel owner- Here’s the rub the insured value was shared by each member and a ‘Call’ (Monies requested up a a maximum per member previously agreed) was made to each member and the total paid out to the affected vessel owner. The only annual fee was running costs for the mutual company and its professional staff and assessors: Are you following me so far? Now if the loss or cost incurred to that or any other vessel was great then the declared Mutual insurance company limitations: Then on behalf of all the companies vessel owners in the ‘Mutual’ then the Mutual Insurance company went to the Insurance Market and insured for the top up amount, based on experience of current costs with Lloyds of London, and further more if the vessel was outside this limit ( A total constructive loss): Then The Mutual company had another brief for reinsurance with Lloyds to pay for all salvage costs.

What one has to realise in that being part of the ‘Mutual’ one had to maintain standards of legal requirements and of the utmost integrity- One has to rely on ones fellow mutual partner being as honest and open as you would be?? Trust is essential for all persons concerned! No shisters here allowed???

You may be asking why all this diatribe? Simple we are among the larger population majority the aging population of the UK (Over 55+’s), and with all the noise made by Age concern and others then can these principles be applied to the older generation for household insurances, and maybe other products or types of insurance such as travel for the over 75’s on a UK and worldwide basis, or even the more mundane such as health (Medical and dental).

There are a few names out their RE whom Frizzels (Liverpool Victoria promoted), and simple health. However one has to be aware their products are geared to the open market, and I was just wondering if similar UK based housing associations, and retirement complexes, or similar neighbourhoods or tenancies in a county town, could afford with Age Concern to form a mutual insurance company to help defray the costs to an aging population.

There is one disadvantage, one if one pop’s ones clogs be liable for dues and calls made after death ( Insurance terms maybe up to 3 years), so probate may be deferred?

This is all chewing over the cud, but happy thoughts: would it work? or does one allow the commercial market its ways to perform, and some of the less fortunate be fleeced of monies hard earned.

Thoughts on a postcard please!

Daylight robbery

An interesting subject this ‘Daylight Robbery’: Is it what we anticipate When our original agreement, or contract is not met, as we the customer understand the small print, or is it our lack of faith in declaring openly, what we wish as an agreement or contract? In other words are both parties coming to some form of understanding and questioned the contract sufficiently at the beginning if the agreement/contract has to be invoked?

Is there honesty and integrity on all sides?

One added note of conjecture is the misdirected business etiquette is that the older generation (60+’s) whether asset rich or not cannot afford to lose monies; and are unable to recoup losses easily. This miss conception, and what has taken a lifetime to accumulate, once lost, one does not have the means or natural working life span to recover such losses.

The government, and the UK business interests of the day, and here I include the state/government run/controlled banks must lead and act with honesty and integrity.

Should we all become destitute as the majority of UKplc? (I.e. The over 60+’s) population, I Ask who can support us from our perilous financial dilemma? Who pays the TAXES to finance our foreseeable state assistance?

It is all a short sighted view!!! WE all of us who trade/buy/sell financial products and services need, and I would personally expect integrity and honesty in our dealings with the money we have/invested/income expectations. So that we can all look one and other in the eye and say good morning with a smile: Not a knowing one, but an honest one

Dear JoHN? (tears in my eyes, sobs from my chest!!) I am missing this Sundays epistle for the sermon on the mount? where for art thou Oh wise one??? Sunday 25th. September 2016. I trust you are well? My thoughts and best wishes are with you.!!!